Harmful tax practices (e.g., tax havens, preferential tax regimes, tax rulings) are characterised by the propensity to erode tax bases of other countries which allegedly leads to an undesirable race-to-the-bottom on taxation rates. Action 5 of the OECD Action Plan on Base Erosion and Profit Shifting (“BEPS”), therefore, addresses the detecting and coordinated countering of such harmful tax practices, with a renewed focus on transparency and substance requirements.

Background

In 1998, the OECD Committee on Fiscal Affairs published a report on Harmful Tax Competition (“1998 Report”), with the purpose of developing a better understanding of harmful tax practices around the world. In total, 12 factors were set out in order to determine whether a preferential tax regime could be harmful.

The four key factors are: (i) no or low effective tax rates on movable sources of income, (ii) ring-fenced from the domestic economy, (iii) a lack of transparency and (iv) no effective exchange of information.

Eight other, indicative factors are: (i) an artificial definition of the tax base, (ii) no adherence to international transfer pricing principles, (iii) an exemption for foreign sources of income, (iv) negotiable tax rate, (v) secrecy provisions, (vi) wide network of tax treaties, (vii) promotion of the preferential regime and (viii) encouragement of operations that are purely tax driven.

Also, the creation of the Forum on Harmful Tax Practices (“Forum”), operating under the auspices of the Committee on Fiscal Affairs, was first proposed in this 1998 Report. The 1998 Report was followed by subsequent publications describing the progress that had been made and the steps that needed to be taken next.

BEPS Action 5

In 2013, the work around harmful tax practices was revived with the 15-point BEPS Action Plan. Action 5 of this Action Plan commits the Forum to:

Revamp the work on harmful tax practices with a priority on (i) improving transparency, including compulsory spontaneous exchange on rulings related to preferential regimes, and (ii) requiring substantial activity for any preferential regime. It will take a holistic approach to evaluate preferential tax regimes in the BEPS context. It will engage with non-OECD members on the basis of the existing framework and consider revisions or additions to the existing framework. (numbering and emphasis added)

The Forum is expected to deliver the following outputs, in three steps:

Review of member and associate countries, by September 2014. In a 2014 interim report on Action 5 (the “2014 Report”) the Forum presented a review of preferential regimes in OECD member and associate countries. The criteria from the 1998 Report were applied, as well as the newly developed substantial activity factor with regard to intangible regimes (see below). From the 2014 Report it should be understood that the monitoring of preferential regimes is an ongoing activity.

Strategy to involve non-OECD member/associate countries, by September 2015. In order to avoid non-OECD countries or non-associated countries enjoying a competitive advantage, these other countries should be involved and take up commitments as well. The outcomes of the efforts undertaken by the Forum to achieve this global level playing field will be published in September 2015.

Revision of existing criteria, by December 2015. Even though the deadline is only set in December 2015, much progress has already been made with regard to the revision of the 1998 criteria and the development of a new framework to detect harmful tax practices. The focus is put on requiring substantial activity for benefitting from preferential regimes and making tax-payer specific rulings more transparent.

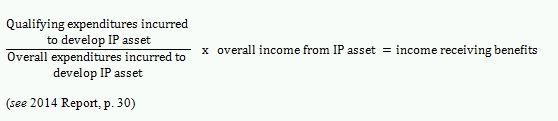

Substantial Activity Requirement in IP Regimes. So far the substantial activity requirement has only been addressed in the context of IP regimes or so-called patent box systems. The main goal is to align taxation (benefits) with substance, which makes it crucial as to how substantial activity is defined. The Forum considers the ‘nexus approach’ the most appropriate: the tax benefits for income from IP-rights only apply to the extent the taxpayer incurred the expenditures to develop this IP-right. In other words, the amount of qualified expenditures incurred by the taxpayer in relation to the total expenditures incurred is considered to represent substantial activity and is used to calculate the tax benefit:

While all expenditures for activities undertaken by unrelated third parties continue to qualify as incurred expenditures, expenditures for activities of related parties are not. The costs for acquiring IP are not qualifying expenditures, while they are included in the overall expenditures.

In the aftermath of the 2014 Report a modified nexus approach was proposed by the UK and Germany. This modified nexus approach reserves the right for corporations using existing preferential intellectual property regimes to still include in the qualifying expenditures the costs incurred by related parties (such as subsidiaries) or the acquisition of IP-rights, it being understood however that such up-lift can be no more than 30 percent of the regular qualifying expenditures. Moreover, it is agreed that no new taxpayers can join any existing regime the moment a new regime is put into place, and neither can new IP assets owned by existing taxpayers benefit from such tax system going forward (relevant end-date will be no later than 30 June 2016). The final abolition date of the old regime would be 30 June 2021.

Improving Transparency Through Compulsory Spontaneous Exchange. With regard to improved transparency, the 2014 Report provides an extensive framework for the spontaneous exchange of country by country tax-payer specific rulings. First, the rulings to which such spontaneous exchange applies are identified. Several criteria are developed, some of which are identical to criteria to detect general preferential regimes. The information on the tax-payer specific ruling should be shared with all the affected countries at the latest within three months after the ruling has become available to the competent authority. The legal basis for this spontaneous exchange will be reported on in the progress report of 2015.

Next Steps

With deadlines approaching in September and December 2015, new interim reports are awaited to gain an overview of the progress made by the Forum on the three outputs it is expected to deliver. With regard to the substantial activity requirement and the modified nexus approach in particular, more details about transitional regimes, reporting requirements, practical methodologies for identifying qualifying expenditures and guidance on the definition of qualifying IP assets are expected. Concerning the compulsory spontaneous exchange of rulings an outline of the application and implementation of the developed framework are expected to come out relatively soon.