Brazilian tax authorities have enacted the regulations for enrollment with the following programs:

(i) the Federal Tax Amnesty Program (“REFIS da Crise”);

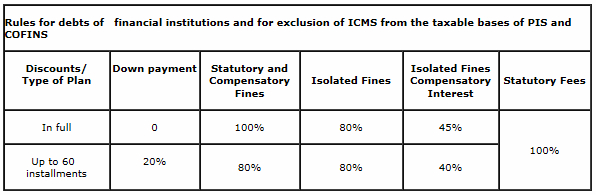

(ii) the incentivized program for payment of Social Contributions on Total Revenues (“PIS/COFINS”) debts by financial institutions and insurance companies with reductions of penalties and interest;

(iii) the incentivized program for payment of PIS/COFINS debts derived from exclusion of the State Value-Added Tax (“ICMS”) in their taxable basis with reductions of penalties and interest; and

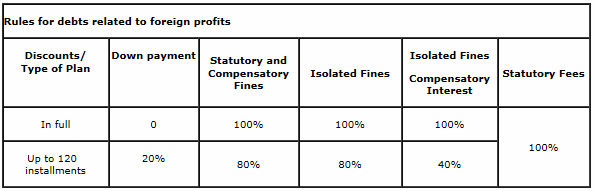

(iv) the incentivized program for payment of Corporate Income Tax (“IRPJ”) and Social Contribution on Net Profits (“CSLL”) debts deriving from disputes related to taxation of profits obtained by controlled or affiliated companies abroad (article 74 of Provisional Measure 2158-35/2001).

The deadline to enroll with REFIS da Crise is December 31, 2013, while the deadline to enroll with the incentivized programs mentioned in items (ii) to (iv) above is November 29, 2013.

According to the new rules, starting from October 21, 2013, the website of the Federal Revenue Prosecutors’ Office (“PGFN”) and of the Federal Revenue Secretariat of Brazil (“RFB”) will receive enrollment requests from taxpayers to REFIS da Crise. The registration to the special installment plans or to the payment in full with the use of net operating losses and negative taxable bases (for the programs that allow for their utilization) will be made exclusively on the website.

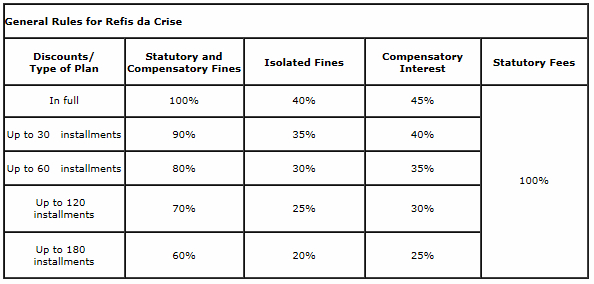

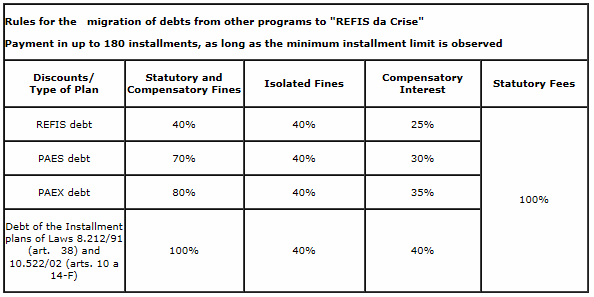

Please find below the applicable discounts related to each program:

November 29, 2013 is the deadline for the declaration of debts of financial institutions and those related to foreign profits and the exclusion of ICMS from the taxable bases of PIS and COFINS that have not been formally included in the Federal Tax Debts and Credits Declaration (“DCTF”). The same deadline applies for the filing of waivers of current administrative and judicial lawsuits dealing with these subjects, if any.

Since the rules of the programs are quite specific, a detailed analysis of each case is necessary before enrolling, especially because the enrollment represents an irrevocable acknowledgment of the specific debt by the taxpayer.